The Looming Retirement Crisis in Five Graphs

A new government commissioned report has outlined some of the key challenges to ensuring people have sufficient resources for retirement in the face of a growing ageing population and changing social conditions.

Elena Boninsegni, our External Affairs Manager for Work, looks at the data to explain what it means for the millions of people approaching state pension age.

In July last year, the government launched the Second Pensions Commission to review the long-term future of pensions and recommend a fair, sustainable system, fit for a changing society.

The new commission comes 20 years after the original landmark review, which introduced major reforms including automatic enrolment, and has been tasked with “finishing the job” of building a pensions system fit for the future. But the economic and social context has shifted significantly since then, with longer lives, weaker wage growth, and changing patterns of work, family life, and home ownership creating a new generation of challenges for policymakers to confront.

This month, the commission published its interim report, with final recommendations expected next spring at the earliest. In this blog, we use five of the report’s most revealing graphs to explore the trends shaping working life today, and what they mean for the future of retirement incomes.

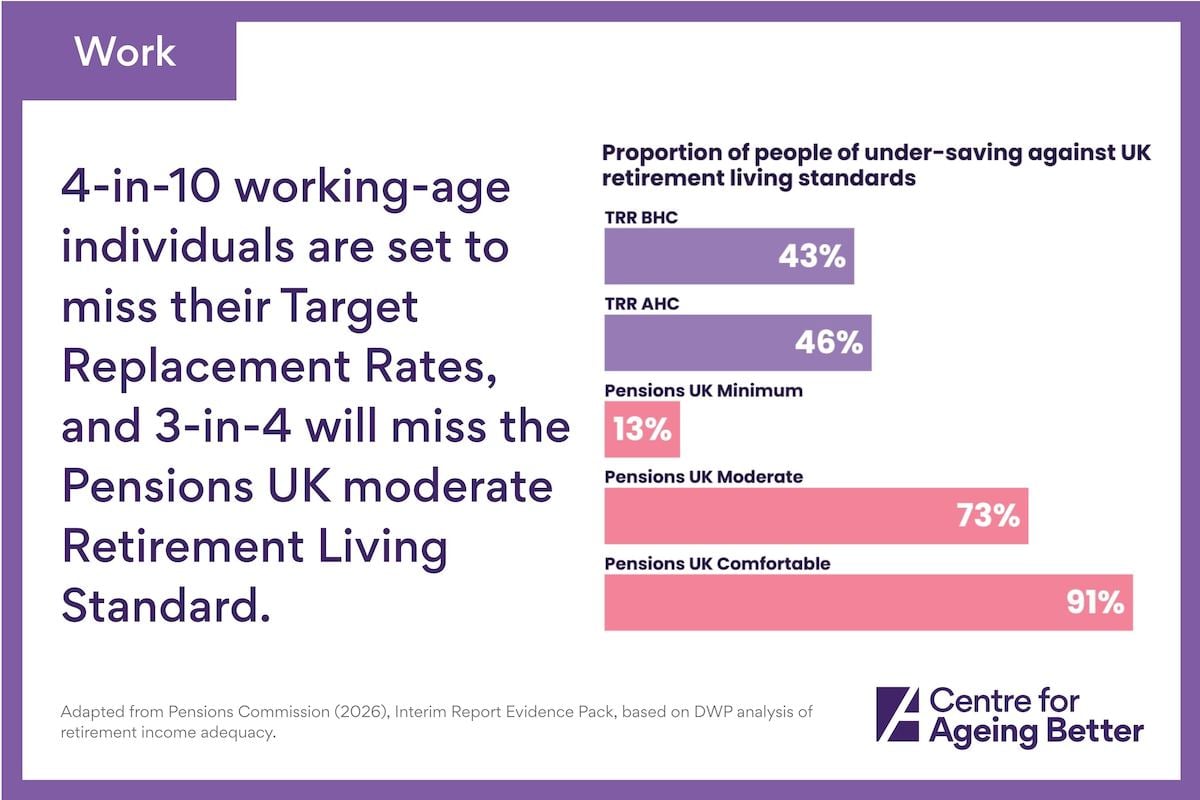

1. Too many people are undersaving for retirement

What does this chart show?

This chart compares how many people are on track to meet different measures of retirement income adequacy. Around four in ten people are not expected to meet target replacement rates, i.e. the percentage of their pre-retirement earnings needed to sustain their standard of living in retirement. The picture is more concerning against broader measures: around three quarters are not on track for a moderate retirement, and in ten fall short of a comfortable standard.

What does this mean?

Automatic enrolment has been one of the biggest successes of the original commission, with nine in ten eligible employees now saving into a workplace pension.

But getting people to save is only part of the story. For many, the minimum contribution levels are not enough to deliver a decent income in retirement, and relatively few people are saving more on top.

The system was designed on the basis that people would build up additional savings alongside their workplace pension and the state pension. In reality, that hasn’t happened at the scale expected. At the same time, other sources of financial security, such as home ownership, have become less certain.

If many people cannot save enough through work alone, then increasing participation will not be enough. The focus now needs to shift towards whether people are saving enough, and how changes in the labour market affect their ability to do so.

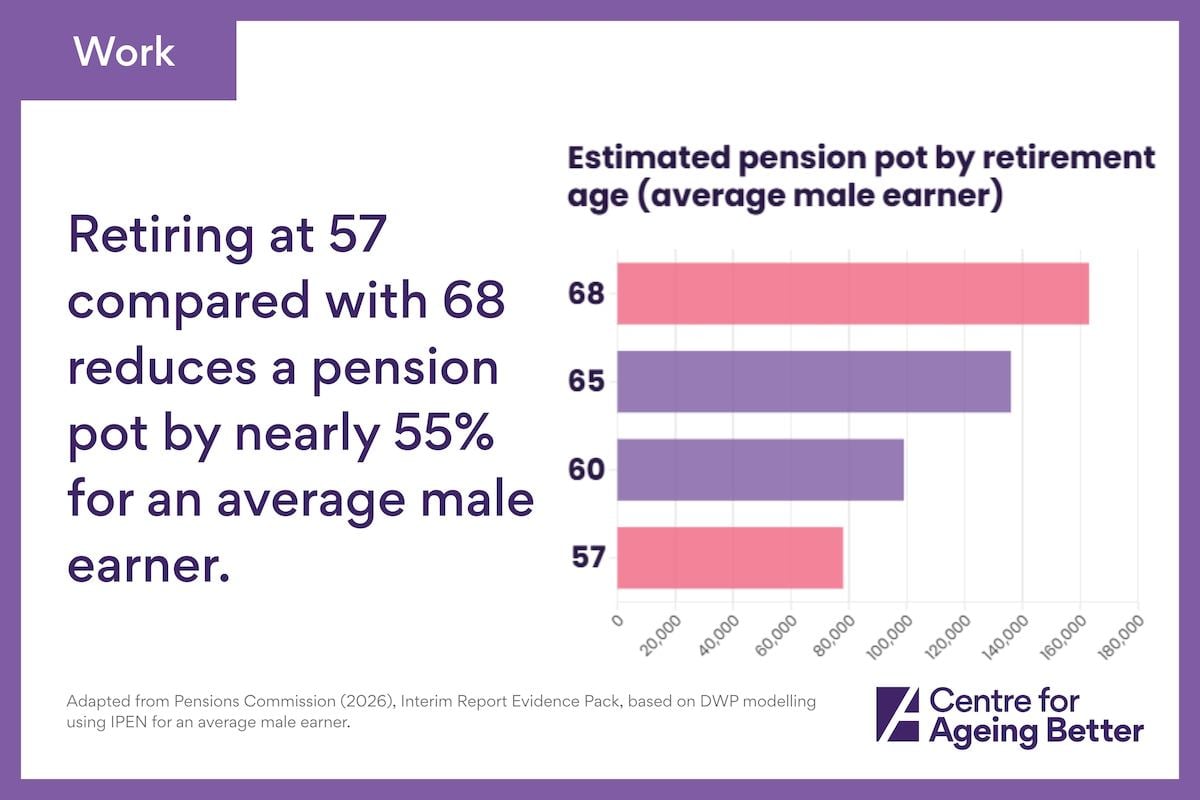

2. Leaving work early has lasting consequences

What does this chart show?

This chart shows how the age at which people leave the labour market affects pension savings and retirement income. For an average earner, retiring at 57 rather than 68 reduces the size of a pension pot by nearly 55%.

What does this mean?

While early career saving is important, leaving the labour market too soon can pose a significant risk to retirement adequacy.

At Ageing Better, our research shows that many people exit work in their 50s not by choice, but due to ill-health, caring responsibilities or limited job opportunities. Once out of work, few fully return, meaning early exits often become permanent.

We estimate that more than 900,000 people aged between 50 and state pension age are currently out of employment but would like to be working. This underlines the importance of creating a labour market that works for people in their 50s and 60s, with better health support, more flexible and secure work, and clearer pathways back into employment.

This will not happen without a targeted intervention. It requires a clear and sustained commitment from government to support this group through an overhaul of employment policy, careers support and the benefits system.

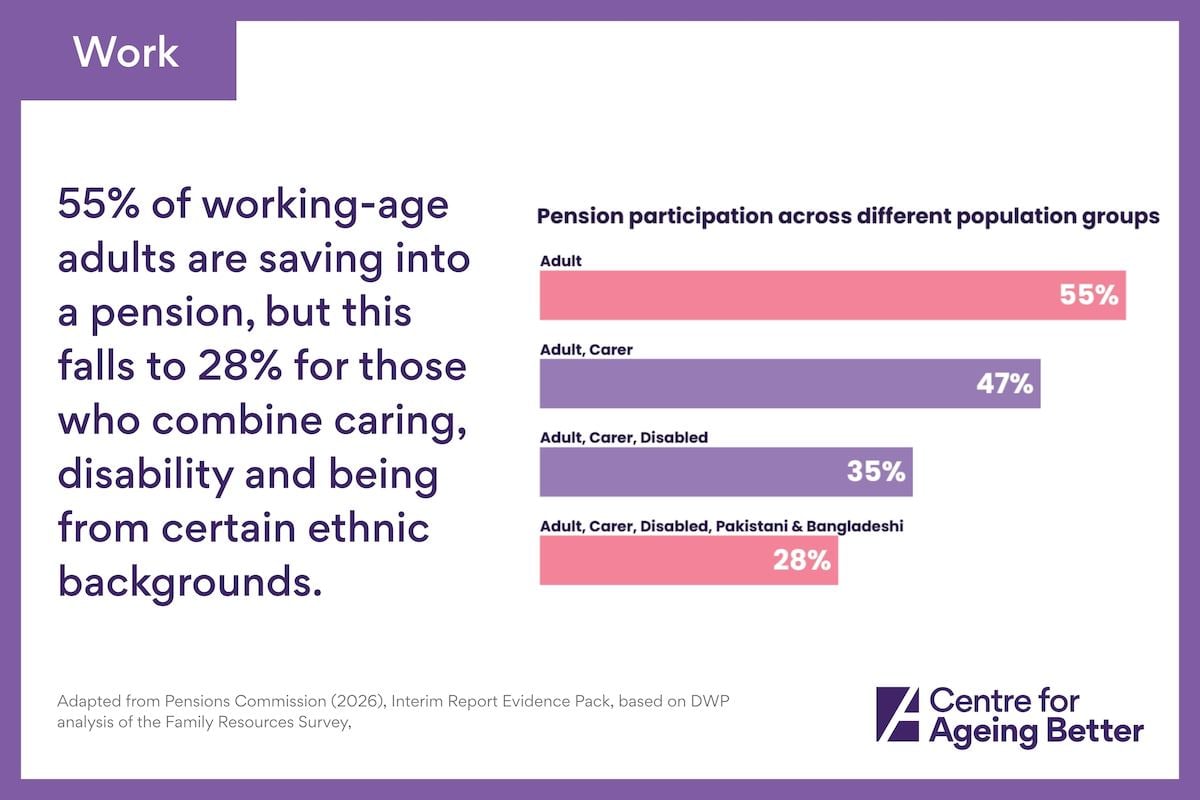

3. Labour market inequalities drive pension inequalities

What does this chart show?

This chart shows how pension participation changes when a combination of different characteristics are taken into consideration. For example, around 55% of working-age adults are saving into a pension, but this falls to 47% for carers, 35% for people who are both carers and Disabled, and 28% for those who combine caring, disability and being from certain minority ethnic backgrounds.

What does this mean?

Pension saving reflects the realities of working life. While automatic enrolment has broadened participation, it has not addressed the underlying inequalities that shape how much people can save.

Lower incomes, insecure work, time out due to ill-health or caring, and limited progression all reduce people’s ability to build pension wealth. Women, Disabled people and people from some minority ethnic backgrounds face particularly high risks of undersaving as a result.

These disadvantages rarely occur in isolation. They often overlap and reinforce one another over time, creating ‘stacked disadvantage’. People facing multiple barriers are the least likely to be able to save consistently and the most likely to see their retirement outcomes fall short.

As a result, those facing the greatest challenges in working life are also those most at risk of inadequate incomes in later life.

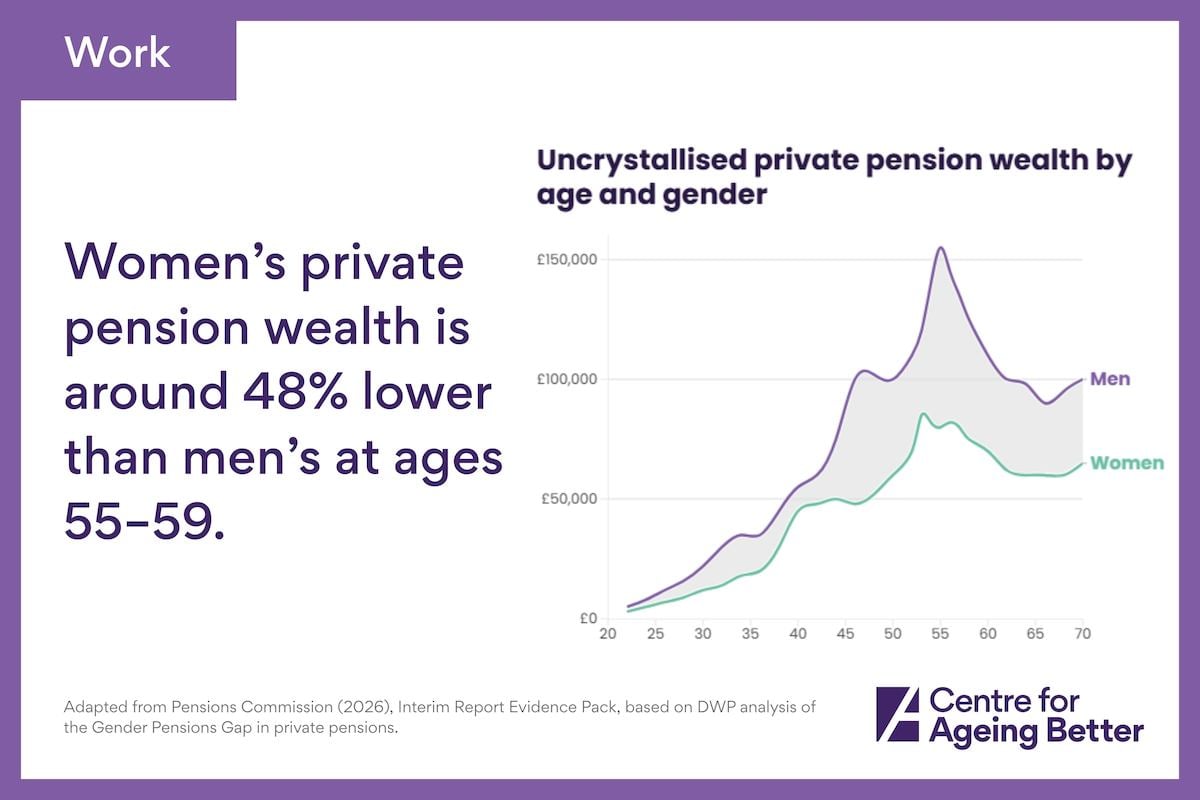

4. The gender pension gap reflects a lifetime of inequality

What does this chart show?

This chart tracks average private pension wealth over the life course, comparing men and women. It shows a clear and persistent gap, which is most pronounced in the late 50s, where women’s pension wealth is around 48% lower than men’s at ages 55–59.

What does this mean?

The UK has one of the largest gender pension gaps in the OECD. This is not driven by a single factor, but by a combination of differences that accumulate over time.

Women are more likely to work part-time, earn less, and take time out of the labour market for caring responsibilities. These patterns reduce both earnings and pension contributions, leading to significantly lower private pension wealth by the time people reach later life.

Reducing this gap requires sustained action across working life, including improving job quality and progression, supporting people to balance work and care, and ensuring that time out of the labour market does not lead to long-term financial penalties.

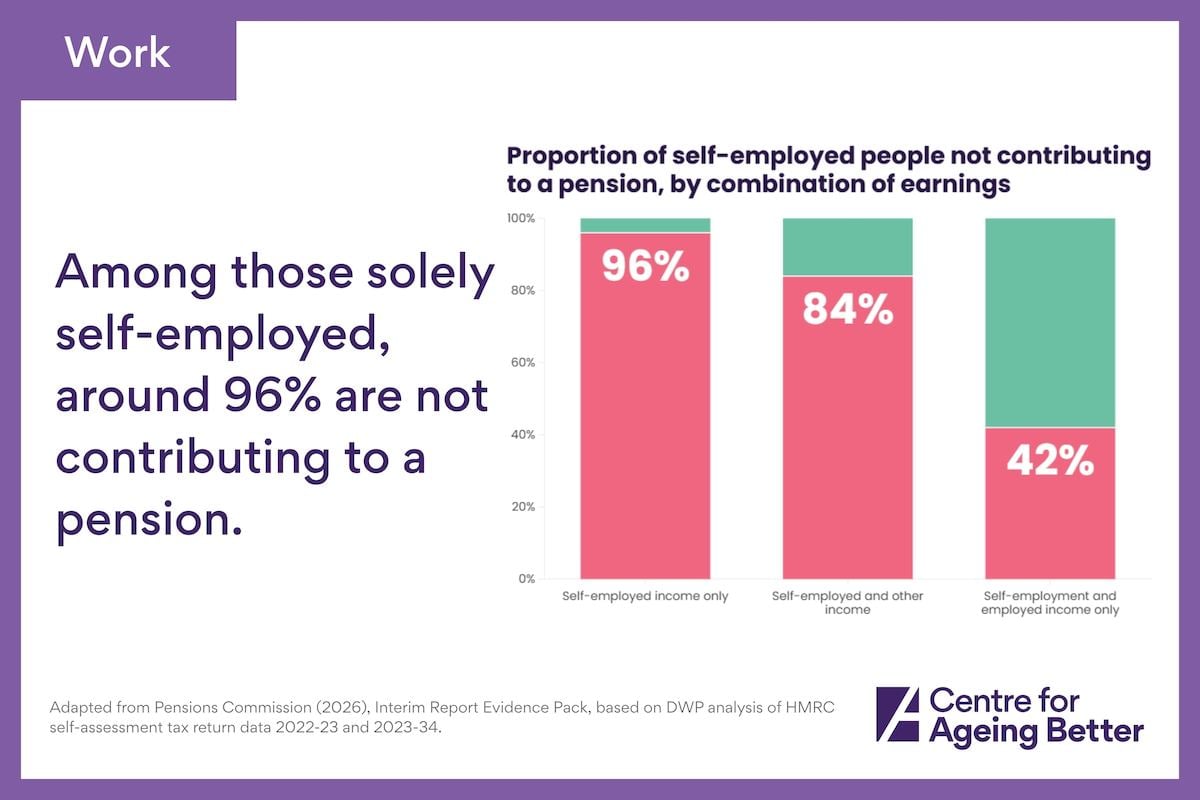

5. The self-employed are at risk of being left behind

What does this chart show?

This chart shows pension participation among self-employed people. Among those solely self-employed, around 96% are not contributing to a pension. Even when including people who receive only a proportion of their income from self-employment , most are not saving.

What does this mean?

Self-employed workers remain outside automatic enrolment and have not seen the same increase in participation as employees.

As a result, many are reaching later life with limited private pension savings. Some may rely on property or inheritance, but these are unevenly distributed and increasingly uncertain.

Without action, a growing proportion of the workforce risks being excluded from the main mechanisms supporting retirement saving. Addressing this will require approaches that reflect the realities of self-employment, rather than relying on a system built around traditional employment.

Conclusion: the need for a joined-up strategy

The evidence is a clear: a conversation about pension adequacy is, to a large extent, a conversation about work. Ensuring people have enough to live on in later life depends not only on the design of the pensions system, but on whether people can build secure, sustained working lives.

This will require a more joined-up strategy. Pensions reform alone will not suffice; there must also be a stronger focus on creating a labour market that supports people to stay in good work for longer. That means addressing the barriers that drive early exits, improving job quality and flexibility, and ensuring that people with health conditions or caring responsibilities are not locked out of employment.

Without this, efforts to improve pension adequacy will fall short. With it, there is a clear opportunity not only to strengthen retirement security, but to support a more inclusive and resilient economy.

Employment and skills support

Find out more