Five million people approaching retirement at risk of not having 'adequate’ pension income

A new report from the Pensions Policy Institute sponsored by the Centre for Ageing Better warns that a growing number of people are at risk of being unable to afford a decent standard of living after retirement.

2 min read

The report warns that the pandemic will further exacerbate challenges for savers and calls for a new settled consensus on retirement income adequacy.

Millions of people in their 50s and 60s are running out of time to prepare financially for retirement, according to a new report by the Pensions Policy Institute sponsored by the Centre for Ageing Better. The report, ‘What is an adequate retirement income?’ estimates that a quarter of people approaching retirement, the equivalent to five million people, are at risk of missing the income they need.

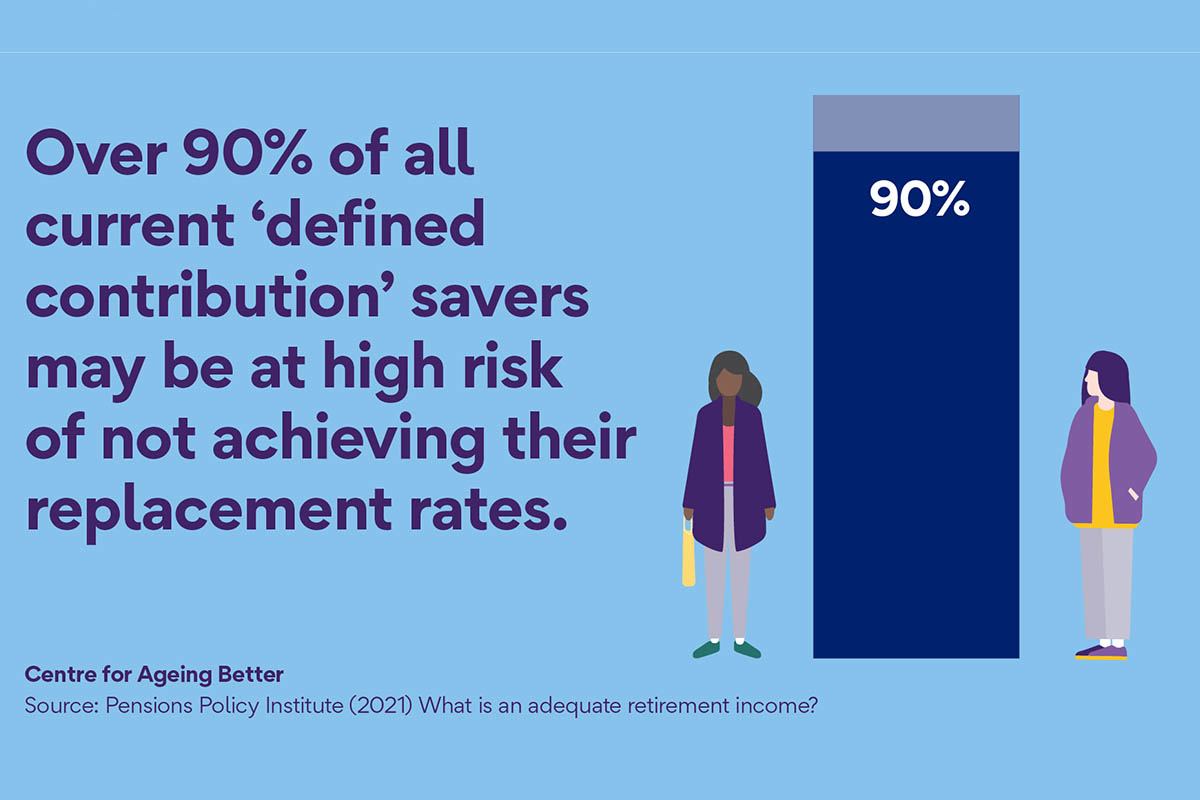

The report finds that a low state pension, increasing unemployment and the transition to workplace pension schemes reliant on employee contributions are all factors leading to a generation being left without adequate savings in retirement. It warns that not only is this an immediate cause of concern for those currently in their 50s and 60s, but that generations to come risk being pushed into poverty if action is not taken to address financial insecurity in retirement. The report found that 90% of people of all ages with Defined Contribution pensions may be at risk of falling short on their expected retirement income.

While recent measures such as auto-enrolment have resulted in more people saving into their workplace pensions, savers aged over 50 spend less time in auto-enrolment schemes and consequently benefit less. Most pension contributions remain inadequate, and challenges for savers have been exacerbated by COVID-19. The report highlights that those aged over 50 had the highest redundancy rate during the pandemic and warns that this age group is more likely than younger groups to experience long-term unemployment. Increasing job losses and unemployment levels may result in the generation currently approaching retirement being pushed out of work and left with a pension that does not provide them a decent standard of living.

The report calls for a new consensus on what adequacy means. As there are various measures of adequacy, the government needs to build a consensus between employers, industry, unions and individual stakeholders on what an adequate income in retirement is. Additionally, Ageing Better is calling on employers to match workplace pension contributions at a higher rate and for better support for groups at risk of financial insecurity.

Anna Dixon, Chief Executive of the Centre for Ageing Better, said:

“The low level of the state pension in the UK, at just 24% of the national average income, means people are unable to rely on the state pension to provide an adequate income in retirement. Many people don’t have enough pension savings to support a decent standard of living in retirement.

“Further action is needed to ensure millions of people approaching retirement and generations to follow do not find themselves without adequate income in later life.

“While auto-enrolment is boosting the number of people saving for retirement, it is not sufficient to secure financial security in later life. We are calling on government and employers to do more to support people to achieve a decent standard of living in retirement and to boost pension savings for those approaching retirement.”

Have we saved enough? Do people approaching later life have an adequate retirement income?

Read more