Busting the “wealthy boomers” myth

The post-war generation now in their 60s and 70s are often portrayed as wealthy beneficiaries of circumstance. Yet almost one in five live in poverty.

Morgan Vine, of Independent Age, and Dr Aideen Young, from the Centre for Ageing Better, explore what is driving concerning levels of penury among our older population.

The State of Ageing 2023 offers a clear rebuttal of the “wealthy baby boomer” narratives that have become so commonplace in public discourse, fueling intergenerational conflict and resentment towards our older population.

Although it is undeniable that there are wealthy older people, wealth inequality within older age groups is vastly greater than between older and younger age groups.

And just as in every other age group, there are large numbers of older people living financially precarious lives. In fact, 2.1 million people aged over 65 are living in relative poverty in the UK today: that’s almost one in five people (18%) in this age group.

How the numbers in the State of Ageing report play out in real life is older people skipping meals, turning the heating off and wearing woolly hats to bed, as call handlers on the Independent Age helpline repeatedly hear.

Meanwhile, Ageing Better’s analysis of data from the abrdn Financial Fairness Trust found older people skipping visits to the doctor and dentist and not seeing friends and family as often as they’d like because of the financial implications.

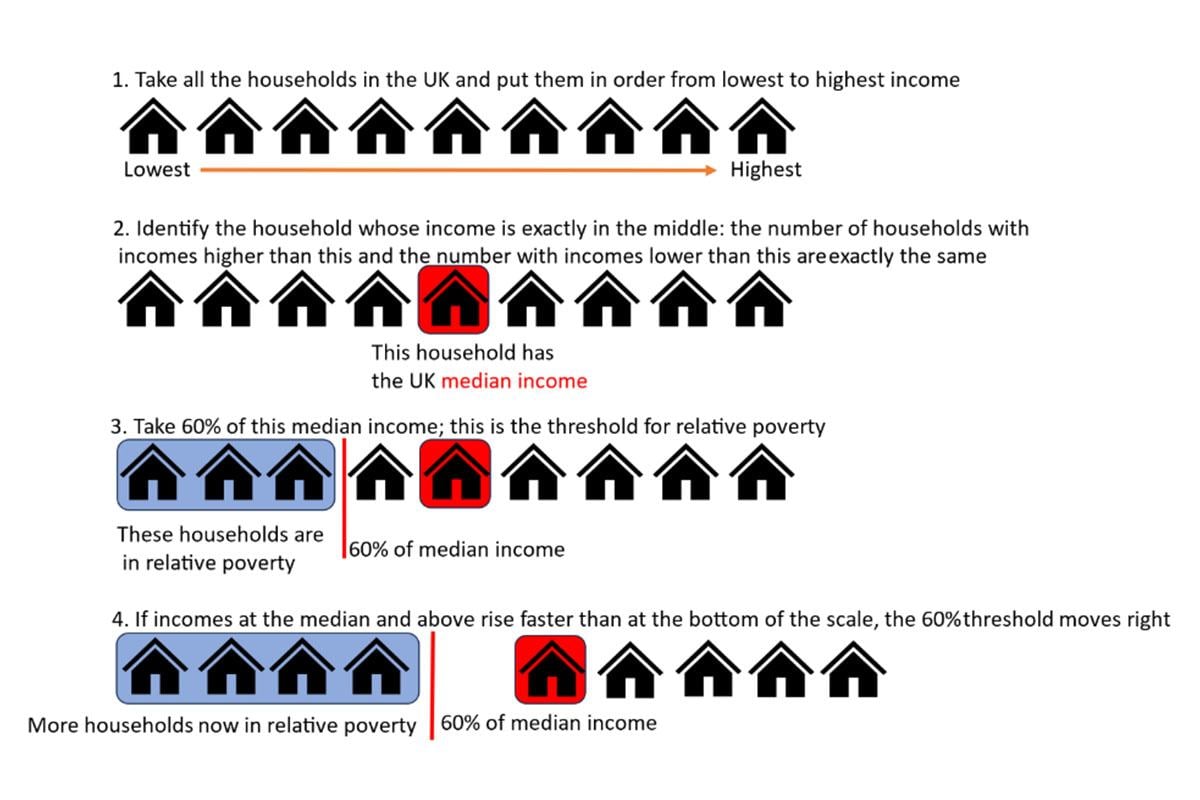

Relative rather than absolute poverty is the preferred measure of poverty because the latter uses a threshold fixed in time rather than keeping up with annual changes. Thus, relative poverty better captures inequality in society and reflects societal and economic shifts. The diagram below shows how relative poverty is calculated:

How does someone fall into relative poverty? Movements in peoples’ incomes – particularly those around the median – cause the median income to shift. If the median shifts to the right, it will bring the 60% relative poverty threshold with it. If incomes at the bottom of the distribution don’t keep up, then more households and more people fall into relative poverty. For those who are economically inactive, and this includes people of pension age, this will happen if the growth in employment income rises faster than the sources that the poorest rely on.

And what are those sources? In the case of the poorest pensioners, more than two in five of whom have no private or workplace pensions, the answer is the State Pension and other benefits.

The issue is that the State Pension, with or without a Pension Credit top-up, gets single pensioners and those in a couple to just 80% of the minimum income standard, a minimum socially acceptable standard of living in the UK today.

Indeed, the UK has among the worst mandatory (state) pension provision across OECD nations. To compound matters, up to 1.2 million people are not claiming the pension credit top-up for which they are eligible.

This is no small matter: research conducted by Independent Age with Loughborough University, using 2017/18 data, shows that 440,000 fewer pensioners would have been in poverty in that period if those who were eligible had received their Pension Credit.

Research by City University of London, commissioned by Independent Age, shows that pensioners living in a household in which social benefit income increased were 20 times more likely to move out of poverty than households in which social benefit income didn’t change.

Alongside this, JRF research shows that three-quarters of people aged 55 and over who were living in very deep poverty (below 40% of median income) moved out of very deep poverty on receipt of their State Pension, and receiving a private pension had a similar effect.

In contrast, increasing the State Pension age by a year to 66 for men and women between December 2018 and October 2020 pushed up the poverty rate for 65-year-olds by 14 percentage points to 24% (or nearly 100,000 people) by late 2020.

The State Pension and benefits therefore play a vital role in keeping people out of poverty.

That’s why we are urging the UK Government to take steps to increase the uptake of Pension Credit, particularly among pensioners from minority ethnic backgrounds who are at a higher risk of poverty.

And we are also calling for a pause in proposals to increase State Pension age, which will, on its own, push even more people into poverty. The next rise in State Pension age to 67 is due to come into effect in just two years’ time. Before more increases are announced we need a cross party agreement on what people need in later life to avoid poverty, and how the individual and the state can work together to make that a reality, including support mechanisms for those without private pensions, savings or assets.

There is significant health inequality in this country which has to be considered too: for example, the poorest women can only expect to live in a state of good health (by their own estimation) to the age of 52, on average. Poor health forces people out of work, putting them at risk of poverty in the years before they get their State Pension. That could be as long as 14 years for the poorest women. Therefore, raising State Pension age across the board would be catastrophic for many.

Reducing poverty also requires rising employment for working-age adults and help with housing costs. Independent Age’s report last year – Hidden Renters - found that almost half (45%) of older private renters have seen a rent rise in the last year. Over half of these (57%) were between £50 and £200. The role of labour market inequalities and our homes in pushing people into poverty in the first place are themes that will be explored in accompanying blogs.

In a country as rich and developed as the UK, it is a source of shame that some of the most vulnerable in society should be permitted to live out their lives hungry and cold. Urgent action must be taken to reverse this trend.